UK projected interest rates in 5 years defy current expectations – Photo: Alexander Spatari / Getty Images

The UK interest rates have risen sharply in 2022 to combat soaring inflation. Yet as the energy prices and supply pressures start to ease in 2023, is it time for the Bank of England (BoE) to start cutting, or at least keep the UK interest rates on hold?

Here we take a look at the projected UK interest rates in 5 years, and what factors may shape them in the long-term including inflation, economic growth and the labour market.

What is the Bank of England (BoE)?

The Bank of England (BoE) is the central bank of the United Kingdom. Founded in 1694, it is the second-oldest central bank in the world after Sweden’s Sveriges Riksbank.

The BoE was founded as a private bank to the government and established by a royal charter granted by King William and Queen Mary in 1694.

The bank’s main purpose at the time was to raise £1.2m in loans for the government to finance the war against France. More than 1,200 people bought the ‘bank stock’ (shares) issued by BoE, making them the first shareholders.

They came from a variety of backgrounds, trades and professions, including carpenters and grocers, merchants, doctors, knights and royalty. King William and Queen Mary, too, were among the original stockholders.

As a central bank, the BoE’s primary mandate is to keep prices stable by making sure that inflation stays at 2%. To do so, the BoE changes its key interest rate, known as the bank rate, to control inflation.

The job of adjusting the bank rate is in the hands of the Monetary Policy Committee (MPC), which consists of nine members – the governor; the three deputy governors for monetary policy; financial stability and markets; and banking.

There is also a chief economist, and four external members, who are appointed directly by the Chancellor of the Exchequer – the second most important member of the cabinet after the Prime Minister.

Members of the MPC are appointed for a set period and may be replaced or reappointed. The committee makes decisions on what monetary policy action to take eight times a year, or once every six weeks.

Other BoE functions include producing bank notes, supervising payment services, and regulating and supervising major banks and other financial institutions, such as credit unions and insurers.

The BoE also manages the UK’s gold reserves and gold held by other banks. BoE vaults contain approximately 400,000 gold bars.

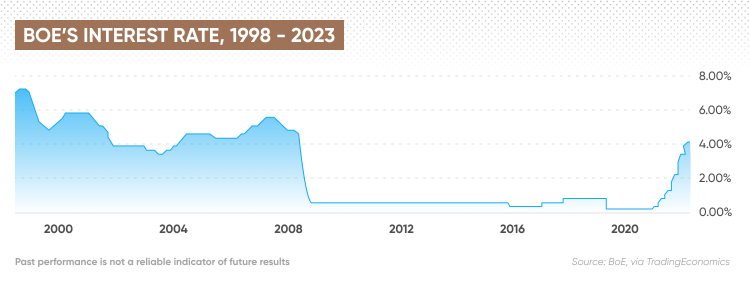

UK interest rate history

The Bank of England interest rate history shows that the bank started to aggressively cut its key interest rate in February 2008. The effect of the global financial crisis, which started in the US with the housing market bubble in 2007, had begun to hit the UK economy.

Over the course of 2008, BoE made five rate cuts, which dropped the rate from 5.25% in February to 2% in December, a level last seen during banking crises in the 1880s and 1890s, according to the International Monetary Fund (IMF). It was also the lowest level in the BoE’s interest rate history since the Great Depression and World War II.

In March 2020, BoE implemented two interest cuts – on 11 and 19 March – which brought the UK interest rates to an all-time low of 0.1%. The BoE’s steep rate cut followed in the footsteps of other central banks and governments that rolled out emergency measures to help their economies weather the pandemic.

First bank rate increase post-pandemic

The near-zero rate was kept until December 2021 as the UK and other countries gradually reopened their economies.

As inflation rose in line with recovery, the BoE increased its bank rate to 0.25% on 16 December 2021 from the low of 0.1%. The UK became the world’s first leading economy to increase its interest rate after the pandemic.

Rebounding demand as the economy gradually recovered from the pandemic, combined with soaring commodity and energy prices resulting from Russia’s invasion of Ukraine at the end of February 2022, has accelerated the pace of price increases.

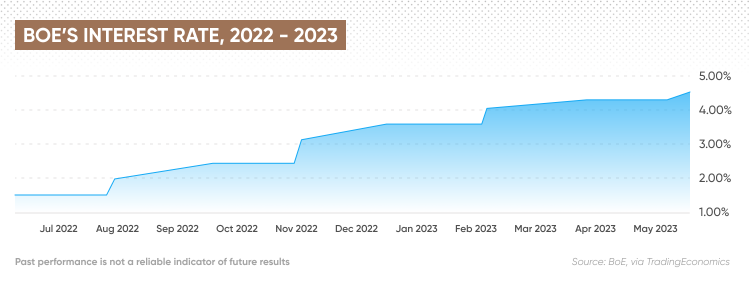

In 2022, the BoE hiked rates eight times, bringing it to 3.5% by the end of year. In 2023, the UK central bank hiked rates once again by 50 basis points (bps) to 4% in February, by 0.25% to 4.25% at the March meeting, and by another 25 bps in May, leading the rate to 4.5%.

Has UK inflation peaked in 2022?

Inflation is likely to be the primary factor that dictates the UK’s key interest rate in the short to medium term.

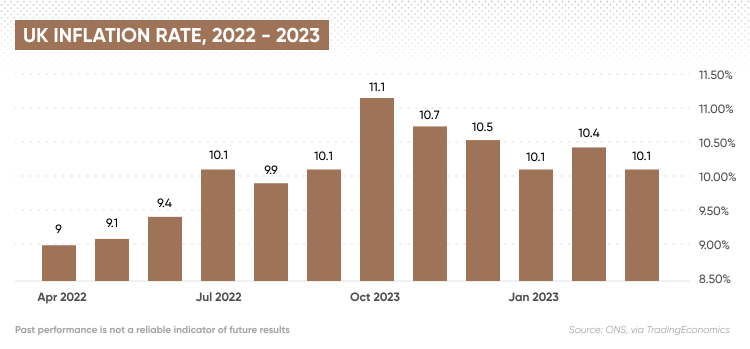

The UK inflation has accelerated in 2022, with the consumer price index (CPI) peaking at 11.1% in October 2022. After slowing down at the end of the year, the CPI unexpectedly edged higher to 10.4% in February driven by cost of foods and non-alcoholic drinks. The inflation has since slowed to 10.1% in March.

In its latest May Monetary Policy Report the UK central bank said that it expected inflation “to fall quickly” in 2023”:

“We expect inflation to fall quickly, to around 5% by the end of this year. While it is likely that the prices of some things such as food will be rising faster than this, energy bills should come down as gas prices have fallen a lot recently.”

The BoE expected inflation to keep declining and meet the 2% target in late 2024.

The British pound (GBP/USD) has moved sideways against the US dollar for the first two months of 2023 caught in between the Fed’s and BoE’s monetary policy. Since March, however, the British currency edged slightly higher, trading with over 4% year-to-date gain as of 12 May.

Labour market remains tight

The BoE admitted that “although there are indications that the labour market has, employment growth has been stronger than expected and the path of unemployment is projected to be lower than in the February report.”

The bank continued: “The UK economy is judged to have been in excess demand over recent quarters, but a degree of economic slack is expected to emerge from the end of this year.”

The latest report by the ONS showed that almost a third (31%) of businesses with over 10 employees were struggling with worker shortages. Meanwhile, 14% of smaller businesses and 23% of businesses with 10+ employees said their workers’ hourly wages rose in March 2023 compared with the prior month,

The UK unemployment rate increased to 3.8% in the quarter to February 2023. Previously, it remained at 3.7% between November 2022 and January 2023, largely unchanged from the previous quarters, and lower than pre-pandemic.

UK economic growth shows signs of stagnation

Gross domestic product (GDP), a key indicator of the health of the economy, is another figure closely watched by the BoE when deciding its monetary policy stance.

The latest ONS data showed that UK monthly GDP fell by 0.3% in March 2023, after stalling in February.

Meanwhile, In the May Monetary report, the UK central bank said that it expected the GDP to be flat over the first half of 2023, “although underlying output, excluding the estimated impact of strikes and extra bank holiday, is projected to grow modestly”. The bank added:

“Economic activity has been less weak than expected in February, and the Committee now judges that the path of demand is likely to be materially stronger than expected in the February Report, albeit still subdued by historical standards. The improved outlook reflects stronger global growth, lower energy prices, the fiscal support in the Spring Budget, and the possibility that a tight labour market leads to lower precautionary saving by households.”

Projected interest rates in 5 years in the UK

In terms of the UK interest rate forecast for the next 5 years, the BoE itself gave forecasts as far as 2026 in its May report.

The bank saw interest rates at 4.4% (lower than the current rate) in the second quarter of 2023, where the rate was projected to stay in Q2 2024, before falling down to 3.8% in Q2 2025. In 2026, the bank saw the rate at 3.6%.

In its UK long-term interest rate forecast as of 12 May, ING saw policy rates staying at 4.5% throughout 2023, until the second quarter of 2024, when it predicted rates to be cut to 4%, followed by cuts to 3.5% and 3% in the following quarters. In 2025, the bank saw UK interest rates at 2.5%.

Echoing this sentiment, Scotiabank’s forecast as of 28 April showed interest rates at 4.25% in 2023, and at 3.25% in 2024.

| 2023 | 2024 | 2025 | 2026 | |

| BoE | 4.4% in Q2 | 4.4% in Q2 | 3.8% in Q2 | 3.6% in Q2 |

| ING | 4.5% | 4.5% in Q1; 3% in Q4 | 2.5% in Q4 | |

| Scotiabank | 4.25% | 3.25% |

Source: BoE, ING, Scotiabank

The bottom line

Analysts mentioned in this article predicted that the rate may peak at around 4.25% (the current level) before easing in 2024 and falling further into 2025 and 2026.

Remember that analysts’ predictions can be wrong. You should always conduct your own due diligence before trading, and never invest or trade money you cannot afford to lose.