Euro paper money and coins – source: gettyimages

As the past few weeks have been dominated by headlines on the evolution of the Hamas-Israel conflict, the focus shifts back to the economic calendar this week with the release of flash PMIs, US GDP and US PCE data. Aside from these releases, the central bank calendar also comes back into focus as the Bank of Canada and European Central Bank kick off the next round of monetary policy meetings.

BANK OF CANADA – Wednesday 25th October

The Bank of Canada (BoC) will be meeting on Wednesday afternoon (15:00 BST) for its seventh meeting this year. So far, the bank has hiked 10 times since March 2022, taking the rate from 0.25% to the current 5% reached in July this year. Since reaching this level, the BoC kept rates unchanged at the September meeting and, according to Reuters data, markets are now pricing in an 87% chance that rates are kept on hold again.

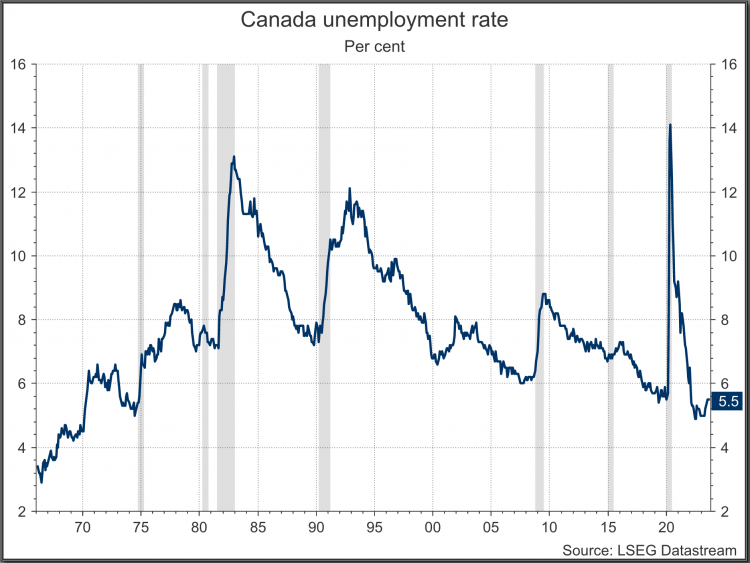

The latest data suggests that the Canadian economy has started to cool. Growth in the second quarter stagnated, dropping from 0.6% in Q1 down to 0% in Q2, below expectations of 0.3%. On an annualised basis, GDP has dropped 0.2%, the first negative quarter since 2021. The labour market has remained somewhat resilient, with the unemployment rate ticking up slightly to 5.5% during the summer but holding below its long-term average. Elsewhere, manufacturing sales have slowed, and retail sales have started to decline on a monthly basis.

Canadian unemployment rate. Source: refinitiv

Consumer inflation (CPI) – the most closely watched data globally for the past 18 months – is back on track towards the 2% target, dropping to 3.8% in September despite expectations for it to remain unchanged at 4%. Since reaching the highs above 8% last summer, CPI had been showing a pretty convincing pattern of disinflation, reaching a two-year low at 2.8% in June, prompting the BoC to keep rates on hold at two consecutive meetings earlier this year. But like what has happened in other economies – including the US – CPI picked up pace once again throughout July and August, which saw another two hikes from the central bank to the current rate of 5%.

The fact that CPI dropped again in September has helped shape expectations that the BoC may continue to hold rates for the foreseeable future, especially if the data continues to show that the Canadian economy is facing a period of limited expansion. The odds for a 25bps hike after the 6 September meeting were hovering around 60% as the BoC stated it was “prepared to increase the policy interest rate further if needed”.

Market reaction to the decision may be limited if it falls in line with expectations. But the press conference – which will be held an hour after the decision and statement are released – may shed further light on the future of monetary policy and the rate curve. Pricing by Reuters shows another 11 basis points implied by March next year, with a 34% chance that rates could be hiked another 25bps by then. This is likely to change after the press conference on Wednesday as markets get a better understanding of the BoC’s views on the recent data, but also the risks that current geopolitical tensions could pose in the future – if any.

It’s also important to note that Canadian bond yields have tracked their US counterparts higher, and while the BoC hasn’t been as vocal as the Federal Reserve on the impact higher yields have on monetary policy, it’s likely that they intend to allow these higher yields to play their part in tightening financing conditions. This would push back the likelihood of more rate hikes, but would likely lead to a sustained “higher-for-longer” rhetoric to avoid repricing in fixed-income markets.

The Canadian dollar – also known as the ”loonie” – has held its ground against the US dollar for most of 2023, with USD/CAD hovering just above the opening level for the year. The rise in US yields – which have been dominating market sentiment for the past few months – allowed a recovery in the US dollar from the summer lows, taking USD/CAD from 1.31 to the current 1.3690 in the space of three months. With the current geopolitical tensions, it’s hard to envision a significant US dollar selloff – even if the rise in the currency seems overextended – so even if we see the loonie pick up some buying interest after the BoC meeting, it’s likely that USD/CAD could be capped going forward as long-term areas of resistance lie ahead.

EUROPEAN CENTRAL BANK – Thursday 26th October

The European Central Bank (ECB) will be delivering its latest policy updates on Thursday at 13:15 BST. It’s likely that the bank will not rush to make any major amendments at this meeting, opting to hold and wait to see how the latest data plays out. This is what markets are anticipating according to data from Reuters, showing a 99.3% chance of no hike as of Tuesday morning.

The ECB delivered a dovish hike in September, taking the deposit rate to 4%, but hinted that this would likely be the last hike for the time being. The takeaway from that meeting was that if the rate was held for a sufficient amount of time at that level, it would make a substantial contribution to the return of inflation to its 2% target. The economic data hasn’t changed much since then. In fact, inflation has continued to decline, dropping to a 12-month low of 4.5% in September, below what analysts had been expecting.

Yields have also risen across the eurozone, which has helped to tighten monetary conditions and strengthen the ECB’s position to hold and wait. The recent tensions in the Middle East have also raised concerns about the already-dampening growth prospects in the region.

But with oil prices having risen since the last meeting, and with the possibility that they remain elevated until risks in the Middle East region dissipate, we may see upward pressures on inflation going forward, which could make the ECB’s life much harder. Prior to the pandemic, most central banks would have deemed a rise in oil prices as somewhat deflationary as it reduced purchasing power and competitiveness. But in the current inflationary situation, where bringing inflation back to target has been a real concern for policymakers, we may see the ECB opting for a higher risk of recession rather than risking their credibility in controlling inflation. This could mean further rate hikes, albeit unlikely at the meeting this week.

This likely means continued hawkish commentary from President Christine Lagarde at the press conference, even if we see no hike this time around. She may opt to place greater emphasis on non-interest rate policy tools to get her point across, including the possibility of a quicker unwind to reinvestments from the Pandemic Emergency Purchase Programme (PEPP).

The fact that the previously mentioned expectations for no hike are so high at the upcoming meeting means there’s likely going to be more emphasis on the press conference than the actual meeting decision. The euro has been showing some resilience in recent weeks, rising to a 5-month high against the British pound (EUR/GBP) and breaking above its descending channel for the first time since it started back in July against the US dollar. EUR/USD is currently reversing some of the moves from yesterday as traders assess the viability of the bullish breakout, but the RSI is still holding above the mid-line, which means the pair could find further support if it holds above the descending channel (currently at 1.0605).