Can the US Fed hold off its planned interest rate rises? Photo: foxaon1987 / Shutterstock.com

The US Federal Reserve (Fed) has raised interest rates by another 25 basis points (bps) at the May meeting, bringing the rate to between 5% and 5.25%, the highest level in 16 years, yet hinting that this may be the last rise.

Is the US central bank done hiking, and what are the projected interest rates in 5 years?

Interest rates and their role in financial markets

Interest rates forecasts have huge ramifications for the wider economy, with decisions by the Fed moving markets across equities, bonds and commodities.

The Fed sets the Federal Funds Rate (FFR), the key base interest rate that filters through to banks, affects demand for bonds and more broadly the economy and stocks.

The process starts when the Fed sets the FFR at the Federal Open Market Committee (FOMC) meeting, eight of which occur every year. Those decisions, which resulted in numerous hikes in 2022, filter through to prime rate, the basic interest rate banks charge to credit-worthy customers.

A hike to the FFR will see the base prime rate rise, affecting the typical cost of loans and mortgages. Increasing the cost of servicing loans takes more discretionary income out of consumers and businesses, dampening demand and reigning in price increases.

For stocks, that could mean companies and stocks dependent on consumer spending, like the retail and hospitality sectors, face headwinds. Growth stocks, which rely on lending and capital, could also suffer as investors look for value in profitable companies to ride out market volatility and a downturn.

Mechanically, interest rate rises also hit the value of bonds. When interest rates rise, the yield on a bond becomes less valuable, as it garners less interest than the prevailing base rate, forcing a sell-off. This is particularly true for longer-term interest rates, as the discrepancy is magnified over time.

Likewise, fixed-income securities lose their value with rises as the cost of not owning other interest-rate tracking assets increases. Indeed, it means the predicted interest rates in the next 5 years could be one of the most telling indicators for markets.

History of the Fed’s interest rate policy

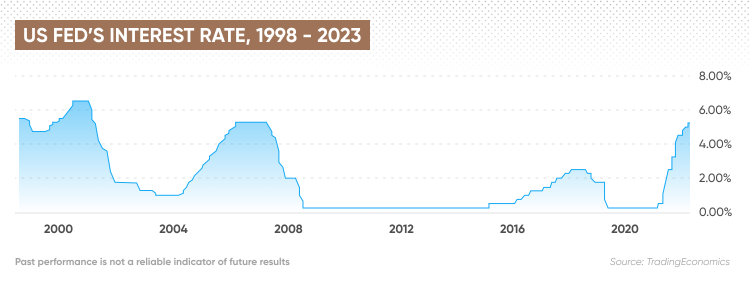

Like other major Western economies, the US has enjoyed an unparalleled period of low price and interest rate volatility. The FFR was at a pretty low rate of under 2% in the 1950s, amid the postwar stimulus and income growth across the US. The rate see-sawed over a 20 year period, rising and falling between 3% and 10% during the 1960s and 1970s, before skyrocketing inflation that exceeded 13% in 1980 forced rates to a record high of 19.1%.

As inflation was brought under control, the FFR hovered around 5% through the 90s, before recessions in 2001 and 2008 forced them down to a floor, keeping rates down until 2016.

The Covid-19 pandemic imposed another cut to almost 0%, with recent inflationary pressures forcing the Fed to begin tightening policy. The Fed increased rates seven times in 2022, and so far three times in 2023, bringing the rate to between 5% and 5.25%, the highest level in 16 years.

Key factors that could influence interest rates in five years

The Fed is now at the whim of greater market forces as it tries to steady the economic ship. Rising prices and an economic slowdown conspire with supply chain holdups to make the outcome of any policy response uncertain. Inflation, and the chances of a recession, will be top of the list.

Slowing inflation

Inflation is the main driver of anxiety in markets and the key catalyst for central bank action. In 2022 and 2023, the source of inflation was a mix of demand and supply factors, but not always interconnected.

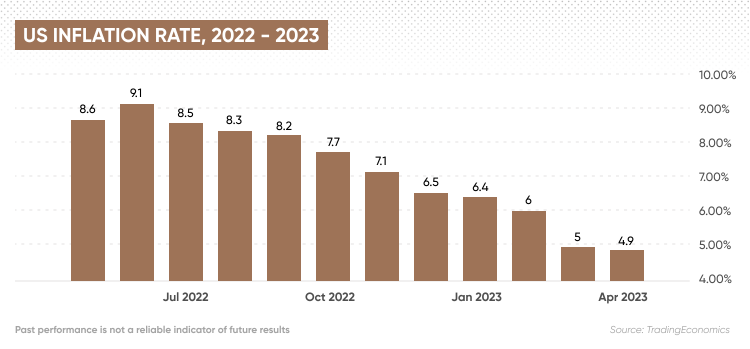

It seems like the Fed’s hawkish policy has at least in part been responsible for a climbdown in the rate of price increases. At the latest May meeting Fed’s chair Jerome Poweel said that the central bank no longer anticipates additional rate hikes, yet he refused to rule out further action as the bank is driven by incoming data. The change of rhetoric may be due to the slowing inflation, which fell to 4.9% in April, the 10th consecutive monthly decline since the 9.1% peak in June 2022.

Amid heavy economic turmoil, the dollar has enjoyed huge resilience. The greenback’s appeal as a safe haven currency, coupled with increased investor attraction thanks to the Fed’s hawkish monetary policy, has helped it outgain most currencies this year.

Yet as the Fed’s monetary tightening has slowed to 25bps monthly and is potentially put on pause, the USD strength appears to be losing steam. In 2023, the dollar index (DXY) moved largely sideways, falling by 1.43% year-to-date, as of 12 May.

Is recession coming to quell the hawks?

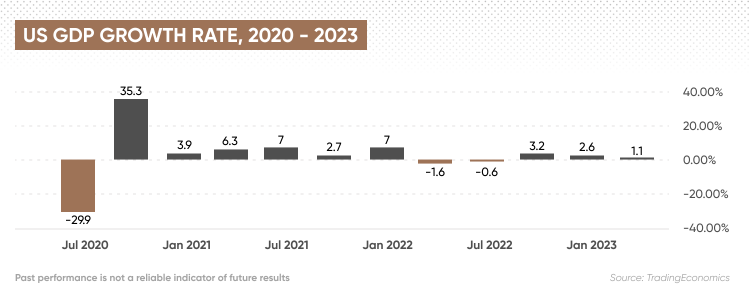

To effectively slow down inflation without affecting economic growth is a balancing act, and the Fed seems to have at least somewhat succeeded. The US economy is not in a technical recession, yet the growth has been slowing in the last three quarters. The US gross domestic product (GDP) has increased by 1.1% in the first quarter of 2023, lower than 2.6% and 3.2% in the quarters before.

The state of the economy is key for the Fed’s decisions and will be watched by its economists closely. Meanwhile, the US recession is a hot topic as the government is struggling to agree on a debt ceiling.

Projected interest rates in 5 years

Analysts typically focus on the near term. Long-term interest rate forecasts stretch into next year and over the next 10 Federal Open Market Committee (FOMC) meetings. They provide insight into interest rate forecasts over 5 years.

An interest rate forecast by Trading Economics, as of 12 May, predicted that the Fed Funds Rate could hit 5.25% by the end of this quarter – a forecast that has been materialised. The rate is then predicted to fall back to 3.75% in 2024 and 3.25% in 2025, according to our econometric models.

In their interest rates predictions as of 12 May, ING saw rates at 5.25% in the second and third quarters of 2023 (a forecast that has been materialised), and falling to 4.25% in the final quarter of the year. In 2024, the Dutch bank saw interest rates starting off at 4% before being cut to 3.75% in Q2 2024, 3.5% in Q3 2024 and 3.25% in the final quarter. In 2025, the bank predicted the rate to decline to 3%.

Meanwhile, Scotiabank predicted as of 28 April the US interest rates to stay at 5.25% for 2023, and fall to 3.5% in 2024.

In the short-term, analysts believed that the Fed is likely to keep the current rate on hold for the near future, provided inflation doesn’t spike again. Daniel Grosvernor, director of equity strategy at Oxford Economics commented on 4 May:

“First, unlike current market pricing, we do not expect rate cuts anytime soon. We believe that the Fed will remain on hold throughout the rest of the year as inflation remains uncomfortably above the 2% target. Indeed, with the FOMC still highly attentive to inflation and data dependent, our macro colleagues argue that there is a risk that the pause proves temporary if inflation surprises to the upside in the next few months.”

Note that the analysts’ interest rate predictions for the next 5 years can be wrong. Interest rate forecasts shouldn’t be used as a substitute for your own research. Always conduct your own due diligence. And never invest or trade money you cannot afford to lose.